PUT Options – Leverage Tool for Value Investors

PUT options are an excellent tool to leverage the realized return for a value investment-based portfolio of securities. In general, options are very risky financial derivatives and are not recommended for unsophisticated investors. In layman’s terms, options are classed as mildly speculative instruments in the world of investing. The key to proper use is to eliminate the risk aspect by only utilizing PUTs in a very restrictive set of circumstances. When properly applied, PUT options can add between four and ten percent of a value investment fund’s annual realized earnings. This marginal improvement is how a value investment fund outperforms even the best-performing index-based funds.

This particular lesson lays out how to properly use PUT options to leverage the performance of an investment fund. First, options are introduced, and why only a particular position with PUT options is utilized. Secondly, a set of highly restrictive conditions is provided that must be followed to practically eliminate the risk options carry for traders of such speculative financial instruments. With this knowledge of restrictive conditions required to use PUT options, the next section explains how they are utilized in a value investment fund portfolio. Finally, several examples are presented to assist the reader with proper application, along with a set of most likely outcomes from employing PUT options.

As with any sophisticated financial tool, an introduction is required.

PUT Options – Introduction to Options and Their Risk Factors

If you have ever watched a sporting event, it is common to see folks involved in ‘Side Bets’. The actual event has its own set of winnings or prestige for whoever triumphs. But spectators often create their friendly bets with others. Thus, the ‘Side Bets’ have nothing to do with the actual event itself. The best way to describe options is to think of them as ‘Side Bets’.

Options are considered financial derivatives. Basically, they are not financial security (notes, bonds, convertibles, preferred, and common stock) issued by a company. They are outside of a company’s financial makeup. Thus, the connection to the principle of a ‘Side Bet’. However, they are monitored and regulated by the Securities and Exchange Commission and the Commodity Futures Trading Commission. In effect, they are regulated and derive their value directly from the financial information provided by the respective companies they are tied to in the market.

With financial securities, the issuing company backs the security by providing different rights or collateral depending on the nature of the security. Naturally, common stock has the least amount of rights or collateral in comparison to secured notes or secured bonds. With common stock, the holder has three key rights.

- First, the holder has a right to their share of dividends.

- Secondly, a shareholder has the right to vote when it comes time to determine board leadership and for certain changes to the charter or policies.

- Finally, a shareholder has the right to sell their security if they want to get out of the financial relationship.

With options, all these rights are nonexistent or highly restricted. Options provide no financial reward from the company; literally, the company doesn’t care about your side bet. Secondly, options provide no rights to vote. As for the third aspect, in some situations, you are indeed allowed to sell your option and get out of the financial deal. Typically, though, this costs money, and unlike securities, where the seller receives money, with options, if one wants out of the deal, one has to pay money.

Notice immediately the much higher exposure an options trader places their investment into when dealing with this type of financial instrument. Simply stated, options categorize one in a much riskier situation in comparison to directly buying and selling issued financial securities. These ‘Side Bets’ can get you into a lot of financial trouble. Thus, CAUTION is warranted. This lesson is designed to teach the reader that only a certain kind of option is utilized with value investing. In addition, this particular kind of option should only be used under highly restrictive conditions. The key is ‘Risk Reduction’.

With this mindset of caution, it is time to introduce the two types of options (CALLs and PUTs) and their respective purposes.

Introduction to Options

CALL Options – this particular side bet is designed to give a buyer the right to purchase a particular stock at a preset price (strike price), no matter what the market price is for the respective stock. It is designed to allow the buyer (holder of the CALL contract) to purchase from the seller of the CALL the stock. Realistically, this would only occur when the market price of the stock suddenly jumps much higher than the strike price. The owner of the call, i.e., the buyer, would naturally elect to exercise this right and purchase the stock for the agreed-upon strike price. In turn, they would sell the stock at the current higher market price and pocket the difference as profit. The seller of the CALL, this so-called side bet, is gambling that the current and future market price will stay the same or go down, and as such will have cash earned from the sale of this call option as additional margin while holding this stock. Take note of the risk involved with the two respective positions of the buyer and seller:

Buyer – Pays a sum of money for the RIGHT to buy this stock at a preset price (strike price) before a certain date (expiration date) from the seller of this CALL. The seller typically owns the particular stock but doesn’t have to own it; they must be willing to buy it at the current market price and sell it to the buyer at the strike price if the buyer exercises the CALL. For the buyer, the risk is that the market price will not surpass the strike price by the expiration date. If the market price does not increase, the buyer’s financial risk is the premium they paid for this right.

Seller – Sells a right to someone to buy a certain stock from the seller at a certain strike price in the future, but before an expiration date. For the seller of this CALL, they firmly believe that the market price will not reach this strike price by the expiration date. The seller’s risk is that the market price for this particular stock soars past the CALL’s strike price and they are forced to sell the stock at the strike price to the current owner (buyer) of the CALL.

Example – Seller (‘S’) owns 100 shares of Coca-Cola stock. The current market price is $62 per share. ‘S’ firmly believes that Coke’s market price will dip or stay at or lower than the current market price for the next three months. ‘S’ sells a CALL option (contract) to anyone for a strike price of $68 per share on Coke for $3 per share, i.e., 100 shares at $3 each or $300. The strike price is $68 per share, and the expiration date is three months out. A Buyer (‘B’) firmly believes that Coke will hit $74 per share within three months. ‘B’ pays $300 to have the right to buy Coke at $68 per share and is willing to wait the three months to see what unfolds. During these three months, Coke’s share price fluctuates from $59 per share to as high as $66 per share. There are now two weeks remaining until the expiration date. This CALL option has dropped in value to 50 cents per share, and the current market price is $66 per share. ‘B’ can continue to wait it out or elect to sell this contract for $50 (100 shares at 50 cents each) and just end up losing $250 in total. ‘B’ elects to get out of the option contract and proceeds to sell it for $50 (50 cents/share). The new buyer (‘B2’) now has a contract with the original seller with two weeks remaining. Suddenly, the market price for Coke soars to $77 in less than three days. ‘B2’ knows a good thing when it happens and proceeds to exercise the option and purchases from the seller 100 shares of Coke for $6,800 (100 shares at $68/each). ‘B2’s total investment into Coke is $6,850 ($6,800 paid for the stock and $50 for the option). The current market price is $7,700; ‘B2’ immediately sells the 100 shares of Coke and realizes an $850 profit from the overall deal. ‘S’ did earn $6,800 from the sale of shares of Coke and also earned $300 from the sale of the CALL option for a total amount of $7,100. ‘B’ lost $250. ‘B’ took a risk and lost some money, and ‘S’ also took some risk associated with the difference between $7,100 and the final market price of $7,700. ‘S’ lost out on $600 had they waited it out. However, ‘S’ is risk-averse and preferred to get their $6,800 plus a $300 premium for selling the CALL option.

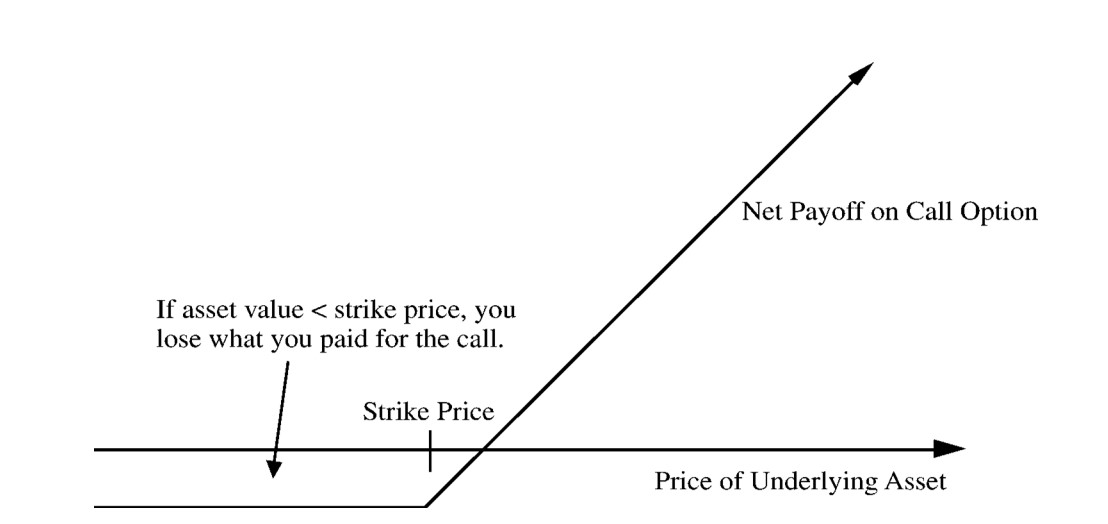

The graph below depicts the overall financial relationship for the two parties. The strike price is the core ‘win’ or ‘lose’ crossover point. On the left of this crossover point of the market price, the seller of the CALL wins the bet outright as long as the market price does not cross over the strike price point. The area between the strike price and where the net payoff line crosses at the market price point is the ‘marginal’ exchange range. Using the example above, this is the $3 range between the strike price of $68 and the value the seller earns of a marginal $3 ($71 market price for the stock). If the buyer exercises the CALL option when the market price is $69.25, the seller earns $68 for the sale of the stock plus $3 for the sale of the CALL. In this $3 zone, the seller is technically the winner of the ‘side bet’. As the market price transitions past $69.50 per share, the buyer of the CALL now begins to gain a better overall financial situation. The buyer is still paying more overall in this transition zone, as the total cost of $71 still exceeds the market price value. But once that market price exceeds $71 per share, the buyer of the CALL is in a superior financial position and is now winning the bet.

One final pertinent part of this overall situation. The exercising of the option only occurs if the buyer is going to sell the security to a third party to reap the reward between their cost of $71 (the price paid for the stock and the option). It is rare for the buyer to exercise the option and then just hold the security. They can do this, especially if there is a significant dividend announcement during this time frame. While the market price is in that ‘marginal’ zone, the buyer’s risk is elevated as it becomes difficult to decide the best course of action; does the buyer wait or act? This is where adequate information as to what is happening not only in the market, but within the industry and at the company level comes into play. In most cases, unless there is a sudden dramatic price increase in the securities market, buyers opt to wait it out. Time benefits them. As the price transitions through this ‘marginal’ zone, if the expiration date is not close, waiting is prudent. After all, this is what the buyer desired when paying for this option.

“Option Pricing Theory and Models” – Chapter 5

Neither ‘B’ nor ‘B2’ is obligated to buy the shares from ‘S’; the option contract is a RIGHT to buy them. ‘B’ or ‘B2’ could at any time, no matter what the market price is, elect to buy the shares at $68 each. Even if the market price is $66 per share, the buyer can elect to buy the stock right then. Of course, a prudent money manager would not do that, but they still own the right.

The one party at most risk of financial loss is, of course, the seller of the CALL option. They may be forced to sell that stock and lose out on all that upper market price range (the area exceeding $71 per share in value in the graph above). Thus, sellers of CALLs risk significant POTENTIAL reward if the market price jumps. In effect, a seller is exchanging potential high reward for a more secure financial position, in this case $68 per share. Both buyers, ‘B’ and ‘B2’, risked the market price decreasing and, as such, only risked their investment into the option contract; i.e., their maximum financial risk is the amount paid to buy the CALL. Think of it this way, they are leveraging their bet with a little money that the particular stock will suddenly soar in value (win the game and hopefully win big) and get a high return on their overall small investment. Remember, they will have to put out money to buy the shares, but immediately, they will turn around and resell those shares at this current high market price.

PUT Options – With CALL options, the primary driver of value is the overall belief in the market price increasing for the underlying security. The price of a call goes up as the market price for the underlying security goes up. This is the opposite for PUT options. PUT values are driven by a decreasing market value.

With PUT options, the typical buyer already owns the stock and is fearful that the stock’s market price will decline over time and therefore wants to force another party to buy this stock from them at some floor value; a value they are willing to tolerate. This strike price guarantees the holder of the PUT a minimum market price in case of a sudden or slow market decline for the respective stock. For the seller of a PUT option contract, they firmly believe the market price is currently stable or will recover for the respective stock and, as such, are gambling that the buyer of the PUT will not exercise the contract and force the seller of the PUT to purchase the stock from the buyer (current contract holder). Review the positions and thought processes of the two respective bettors:

Buyer – Owns stock in a particular company and wishes to eliminate their downside risk; i.e., the stock’s market price will drop dramatically or slowly decline over an extended period. As such, the buyer of a PUT option contract is willing to pay some kind of premium to minimize their potential losses. The closest comparable financial instrument is insurance. With insurance, the asset owner (auto or home, as an example) fears that the value will suddenly drop due to some unforeseen accident and, as such, is willing to pay for insurance to protect that potential value loss. With financial security, the asset owner is buying a PUT option, a form of insurance, to protect against a sudden or extended market price decline for the asset they own. Note that with typical insurance, insurance protects against acts of God or acts of physical mistakes (auto accidents). Insurance does not protect against declines in market value for a home or auto. PUT options are designed to act as insurance against value decline for the underlying security instrument.

Seller – Firmly believes the market price for a particular security will not decrease but either stabilize or improve over time, and is willing to sell an option to earn some money. The seller sets the strike price well below the intrinsic value of the underlying security involved. This reduces the chance that the particular security will continue to decline in value over time. As an example, look at this pricing structure for a PUT option on The Walt Disney Company. The intrinsic value is estimated at $116 per share, and the current market price is at $100 per share; thus, the market price is already 14% less than the intrinsic value. The chances that the share price for The Walt Disney Company will continue decreasing are remote. Naturally, there is a greater chance it will decrease to $95 per share than to $90 per share. Thus, the price for a PUT option is more expensive at $95 per share due to the risk it will be exercised at $95 rather than $90 per share.

Notice how even at $60 per share strike price with a three-month expiration date, there is some interest (161 buyers have indicated a desire to buy a contract) to buy a PUT option in the market. These buyers have indicated that they are willing to pay 32 cents per share to have insurance that their Disney stock could be sold to someone if the market price goes below $60 per share. The key to this chart is that there is less and less risk of Disney’s share price continuing to drop further and further, as first, the open interest in insurance wanes and the price buyers are willing to pay drops dramatically too.

Example – Seller (‘S’) is convinced Disney has hit rock bottom in market price due to several underlying reasons. First, it is a rock-solid company and is traded as a DOW Industrials member. Secondly, the company’s revenue and net profits are significant and have improved over the last three years. Third, the real driver of this current decline is the overall mindset in the market, which is experiencing declines. ‘S’ is highly confident that the market price will not dip below $90 per share and, as such, is willing to sell a PUT option contract for 100 shares at $4 per share or $400 for the entire contract. There are currently 2,486 buyers interested in purchasing a contract to force the seller to buy Disney at $90 per share. One of them enters into this arrangement. The buyer (‘B’) purchases from ‘S’ this PUT option. The strike price is $90 per share with an expiration date of 09/16/2022.

Over the next month, Disney’s stock price wavers, ebbing and flowing, and begins to creep back up towards $110 per share. In late July, Disney released their financial results, and to everyone’s surprise, they didn’t perform as well as they predicted. The market price dips to $89 per share. At this point, ‘B’ has the right to force ‘S’ to buy the stock from ‘B’. ‘B’ decides to wait a little longer; after all, ‘B’ has until September 16th to force the ‘S’ to oblige the terms of the contract. ‘S’ isn’t nervous yet because ‘S’ is convinced this is a temporary setback. In early August, Disney released a new Pixar movie, and it became the number one summer hit and earned more than $200 million in one weekend. On Monday morning, Disney’s stock price improves due to this batch of good news and goes back up to $95 per share. The price continues to improve as more good news comes out of Disney’s information center that their subscriptions to their Disney+ channel are exceeding their expectations. The price of Disney’s stock soars to $112 per share and never looks back as the expiration date finally expires. ‘S’ did indeed earn $400 and was only truly at risk for a few days. ‘B’ paid $400 to protect his investment in Disney, and at one point could have forced ‘S’ to buy the stock from ‘B’.

Take note of the financial relationship with PUT options. The seller’s risk only exists if the market price goes below the strike price. Even then, that risk doesn’t exist until the market price drops below the strike price less the sales price of the PUT option. In the above example, ‘S’ isn’t really at risk until the price drops below $86 per share. At that point, if ‘B’ exercises the option, ‘S’ has to pay $90 per share and own Disney. Thus, the total amount out of pocket for ‘S’ is $86 per share ($90 per share paid to own the stock less $4 per share for the option sold). If the market price continues to slide further lower, ‘S’ will experience an unrealized loss for the difference. This is important, ‘S’ has yet to realize an actual loss because to realize an actual loss, ‘S’ would have to sell the stock at a price lower than ‘S’s basis, which is currently $86 per share. ‘S’ can simply wait it out and hope the market price will recover in a short period.

This is an important aspect as a seller of PUT options. As a seller, you only realize losses IF you sell the stock you were forced to buy at a price lower than the net realized basis in your investment ($86 in the above example). Look at this graphical depiction to help clear up this viewpoint:

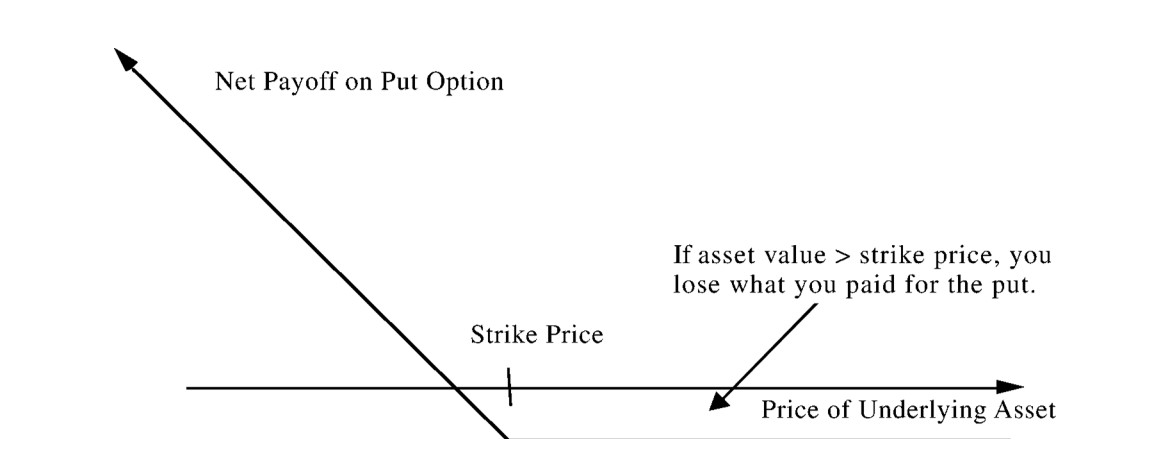

Payoff on a PUT Option

The risk for the buyer is the area to the right of the Strike Price. As for the seller, the risk factor starts when the market price for the security is less than the Strike Price. As the market price crosses over the net realized value (strike price less the value derived from the sale of the PUT – $86 from the above example), the seller’s risk begins to increase financially from zero to the difference between the net realized amount (strike price less sale’s price of PUT options) and the current market price because the current owner of the option may force the ‘S’ to buy the shares at the Strike Price. The further the decline in market price, the more likely the buyer of the option will exercise the agreement and force the seller to pay the strike price.

Remember, the buyer has until the expiration date to force the hand of the seller. It is possible and often common for the market price to dip well below the strike price, and the buyer continues to wait it out. The buyer has time on their side in this set of conditions. Their risk of financial loss is practically zero in this situation, and often they will just wait to see what happens.

Options and Respective Risk Factors

Both types of options are technically side bets in the market. However, unlike a traditional side bet, which utilizes a strong position of speculation due to limited information, options are directly relatable to the underlying asset, i.e., the company in question. Therefore, the speculation element in the decision matrix will match the speculation spectrum of the company under review. Thus, options on large caps and DOW companies are less speculative than options tied to small caps or start-ups. The consensus among unsophisticated investors is that options are highly speculative and therefore dramatically riskier.

In general, options are riskier due to the fact that the buyer and seller are not trading an actual security. This, by itself, moves this particular financial instrument into a riskier territory of investments. But the risk factor for this aspect is tied more to the required knowledge to understand the forces that drive an option’s current market price. Not only must an investor understand the underlying securities’ financial matrix, but the investor must also incorporate the forces that move an option’s market price. An investor must be more sophisticated with these forces of deriving value.

In addition, each of the four possible option positions has its own distinct risk factors. With CALL options, a buyer’s financial risk is strictly limited to the cost paid to purchase the CALL. In most cases, the price of the underlying stock doesn’t soar above the strike price, and therefore the buyer only loses out on the cash paid to buy the CALL. The seller of the call carries a greater financial risk in that if the stock’s price suddenly soars in value, the seller can’t reap those dramatic gains. They are limited to the strike price for the particular stock investment. PUT options also have distinct risk factors for each of the two positions. Sellers are at the most risk because the price could keep falling, and of course, they will have to pay the strike price for stock that the market now deems dramatically less in value. Buyers of PUT options only risk the initial premium paid to own the right to force the seller of the PUT to buy the stock from them.

Thus, both sellers of CALL options and PUT options are at the greatest risk with their respective options. But of course, this makes sense; after all, they are also earning some money from the sale of the respective option and, as such, should have the greatest exposure to risk.

PUT Options – Value Investing Risk Factors

A value investor’s mantra is tied directly to the business tenet of ‘buy low, sell high’. This tenet is focused on four key principles of exercising risk reduction, understanding intrinsic value, conducting financial analysis to sell high, and having patience to allow time to achieve both aspects of buying low and selling high. The primary key driver of realizing good returns with any investment is the ability to buy low. When a value investor determines intrinsic value and then sets a buy price that creates a strong margin of security, such as 15% or more, buying low creates tremendous wealth as time will drive the value of the security higher. The key is to buy well below intrinsic value.

Only as a seller of PUT options can a value investor realize earnings and gain an additional opportunity to buy low. However, this should only be done under the following restrictive conditions:

- The particular PUT option is sold tied to one of the opportunities within a Value Investment Fund portfolio. In effect, this particular investment complies with the risk reduction tools commonly used as criteria for investment opportunities:

- A top 2,000 company;

- Company must be financially stable;

- Company demonstrates good growth beyond inflationary growth.

- The option pricing structure has marginal decreases for significant step-downs in strike price points.

- The underlying company is not currently involved in an intensive stock buyback program.

These restrictive conditions mimic the criteria customarily used for purchasing traditional stock in a value investment portfolio. However, there are a couple of additional restrictions involved:

Pricing Structure Has Marginal Decreases for a Significant Step Down in Strike Price Points

This restrictive condition refers to the marginal loss of revenue from the sale of an option for a decrease in the strike price. Here is that same chart for Disney’s PUT options from above:

Notice the price for a PUT option is $5.60 for a marginal change in the market price of the stock from $99.40 to $95.00 or $4.40. However, the next $5.00 of market price reduction only costs the seller of the PUT a mere $1.60. To go from $95 to $85 strike price, the marginal reduction in the PUT option price dropped $2.86 (from $5.60 to $2.74). Thus, an additional $5.00 of savings from $90 to $85 only costs the Seller another $1.26. The first additional $5 of savings costs $1.60, the next $5.00 of protection costs $1.26; from there, it continues.

This pattern is common with all PUT options for their sales price. Each incremental price reduction costs less and less in terms of the sales price reduction for the option.

For value investors, the secret is to find significant strike price reductions for a very low overall decrease in the PUT option’s price. As an example, look at this schedule for Norfolk Southern Corporation, one of the five publicly traded Class I Railways in North America. Its current intrinsic value is approximately $197 per share. A value investor could achieve a margin of safety of 15% by selling a PUT option at $165 strike price for $2.75 each. Thus, a 100-share PUT option contract will earn the value investor $275 and an opportunity to own a high-quality company paying $5 per year in dividends, earning more than $11 per year on average over the last five years, AND is tracking for $12 of earnings in 2022. The current market price is $220 per share.

At $165 per share, there is a 16.25 % margin of safety over intrinsic value, a $64 margin of safety from the current market value ($229/Share), which exists in a depressed market (Norfolk Southern was trading at a peak of $299 a mere six months ago).

The primary key point here is to notice two distinctly different value points. A seller could sell the option at $175 strike price, which is $5 lower and makes 10 cents more per share! For a marginal reduction of 65 cents per share ($3.40 to $2.75), a value investor can acquire an additional $15 of safety margin. What is more important is that a typical ‘BUY’ point for Norfolk Southern is only 9% safety margin. Thus, this site’s Railroad Pool has Norfolk Southern as a ‘BUY’ at $180 per share!

Imagine the value acquired if a value investor could own this company at $165 per share? It is $15 lower than the set ‘BUY’ price, and at $165, the margin of safety far exceeds the required amount. The likelihood of Norfolk Southern’s market price dropping to $165 per share is so remote that this type of opportunity is simply unheard of in investing. Again, the key is the marginal cost (reduction in the form of PUT option sell price) for dramatic strike price changes; this is what a value investor seeks as a risk reduction tool for PUT options.

What a value investor desires with PUT options is a good return with as little risk as possible. If a value investor is forced to buy the security, at least it is purchased at LESS THAN what is determined to be the preset ‘BUY’ point for that security. This just adds additional protection against further security market price reductions.

Who wouldn’t want to own a top 2,000 company with a 3% dividend yield ($5/YR on a purchase price of $165/Share), earning more than $11 per year with a prior peak market price of $299 per share? This is a solid company.

No Intensive Stock Buy-Back Program

The third restrictive condition for risk reduction with PUT options is the underlying company’s stock buy-back program. Stock buyback programs typically work against intrinsic value determination. Intrinsic value determines the in-house value of the company. Think of it as the value that would exist in the equity section of the balance sheet and would equal the book value of the company’s stock. If a company participates in a buy-back program and pays more per share to buy stock back off the market (Treasury Stock), the company is literally taking existing book value from the remaining shares and giving it away to those whose shares are being purchased. It is an intrinsic value killer. Rarely do highly stable companies trade in the market for less than their intrinsic value. Think about it for a moment; this is why value investors set intrinsic value to determine the real worth of the stock. Value investors are not in the business of buying securities for more than they are worth.

If a company has a stock buy-back program and the company is one of these highly stable operations and included in the value investment portfolio, it means that the intrinsic value is going to go down depending on how much value is shifting out of the company to buy back the stock. Most treasury stock programs are small, and a company is trying to buy back two to four percent of the whole portfolio of outstanding shares in three years. At this level of a buy-back program, the reduction in intrinsic value is relatively low (maybe a net effect of seven to nine percent overall reduction), but it still affects the calculation related to PUT options due to the leveraging concept. Thus, look for programs whereby the stock buy-back is less than two percent of the total outstanding number of shares. If greater, the value investor must look at the impact over the period to the expiration date; how much value will shift out of the company during this time frame?

Continuing with the example above, Norfolk Southern’s buy-back program allows for the repurchase of up to 6 million shares by December 31, 2022, including the six months remaining. The current number of shares outstanding as of March 31, 2022, is 238 million; thus, if all 6 million shares are repurchased as treasury stock, the company’s intrinsic value would drop approximately 2.6% assuming shares are repurchased at more than $220 per share. This means, intrinsic value COULD decrease to $192 per share by December 31, 2022, which covers the open period of this option. In effect, Norfolk Southern’s stock buy-back program (repurchase program) should not impact the decision model related to selling the PUT options with a strike price of $165 per share.

As long as a value investor adheres to the three required restrictions for selling PUT options, the risk factors tied to PUT options can be dramatically reduced or eliminated. The other three remaining positions do not have this ability to utilize restrictions to reduce this risk, and in general, are counterintuitive to what a value investor is about. With this information, how can a value investor properly apply a system of utilizing PUT options to increase a portfolio’s annual return?

PUT Options – Proper Application in a Value Investment Portfolio