Financial Statements (Lesson 10)

Accounting is the language of business – Warren Buffett.

Each year, every publicly traded company is required to report its financial status. Many go beyond simple financial statements and prepare an annual report covering all the relevant issues affecting the company. The high-quality corporations present a fully comprehensive document that covers the prior year’s activity, including impact factors and why there is a difference between what was expected and the end result. In addition, these companies prepare forecasts of production, sales, and any pending changes with systems and production processes. Most importantly, they include key performance data that allows shareholders to have a deep understanding of the economic variables that affect financial results.

But the primary purpose of the annual report is to present financial information. This is where the average non-accountant-degreed investor has trouble. Many are not confident about interpreting and understanding financial statements. Don’t let this lack of knowledge prevent you from pursuing value investing. Understanding financial information isn’t as difficult as one may believe or have been told. In Phase Two of this program, there is a lot more information and exposure to the different ways of interpreting financial results.

To understand financial information, first, the member must understand their general purpose and how they are prepared. The first section of this lesson introduces financial statements and their two primary purposes. In addition, pertinent issues are introduced that a company must address to finally present a well-prepared set of reports. Next, each of the five major types of financial statements is introduced. Most companies present a core set of five that include a 1) balance sheet, 2) income statement, 3) statement of retained earnings, 4) cash flows statement, and 5) a set of notes to clarify the four statements. Some go further and present industry and highly customized financial reports. These are covered in Phase Two of this program, along with the Pool’s information center that members have access to on this website. Finally, this lesson covers the importance of a few key bits of information and how these critical financial values impact the respective buy/sell models that value investors develop.

Many stock market investors are not familiar with financial reports; they rely on accountants to provide the results in layman’s terms in order to make decisions. This program is designed to build the confidence of non-accountant types to not only understand financial reports but to appreciate and ultimately, eagerly await their arrival each quarter. Again, Phase Two of this program goes in-depth about financial statements and how to interpret the information.

The first step with all of this is to be introduced to financial statements and why they exist.

Introduction and Purpose of Financial Statements

Simply stated, accounting is the recording of economic activity. It is done after the fact of the transaction. The entire profession is driven by the proper organization of information. This includes terminology, definition, and, of course, legal compliance. The profession uses a set of rules called Generally Accepted Accounting Principles (GAAP) along with a hierarchy of authority to support and promulgate these rules. As an aside, many non-accountant types do not realize that the recording of data is an in-house process. Furthermore, this in-house team organizes the data and reports the results in the form of financial statements. An outside team, typically CPA’s from an accounting firm, validates the information by performing an audit of the financial information.

An audit means that they tested the data for accuracy and proper organization. In effect, the CPA’s verify that the company followed the rules. If the company followed the rules, the firm would issue a letter that is customarily a component of the cover letter to the section for the financial statements in the annual report. When the report is issued, it typically states that either the information is ‘FAIRLY’ presented or they qualify their opinion. If the firm qualifies its opinion, it will state why it is qualified. The most common reason for qualifying the reports is that the company departed from GAAP in some material way.

Almost every single large-cap and DOW company issues ‘FAIRLY’ stated reports and will not depart from the rules of how data is recorded and reported. If they did, the company would see a sell-off of its stock. Remember what this is about: if you want to play in the big leagues, you must follow the rules. This is another reason why value investing only uses high-quality large corporations for its stock selections. The other tiers have higher risks because many of them have trouble following the rules.

Thus, the primary purpose of financial statements is to answer the question: ‘Did the company follow the rules?’.

Whenever you look at the annual financial statements of any company, your first step is to read the Independent Auditor’s Report. Did the company follow the rules? If not, don’t invest in that company!

For clarification purposes, quarterly reports, i.e., the first three quarters of each fiscal year, are called interim reports. Interim reports are rarely audited. In most cases, these reports have not been looked at by an outsourced accounting firm for compliance.

If the statements are ‘fairly’ presented, then this means the information is organized properly, and as such, this means the information is reliable.

A second purpose of financial reports is that the financial information must be disseminated promptly. The accounting profession has two tenets. The first is referred to as accuracy. Did the company properly record the economic activity, i.e., did they classify the information according to the rules and for proper amounts? Secondly, did the company do this on time?

It does no good to get financial information in a tardy fashion. Shareholders and those interested in buying into a company are eager to get information; so is the Securities and Exchange Commission. The SEC has time compliance requirements for publicly traded companies. In general, companies have 40 days to report quarterly information and 60 days for annual information. Since most companies have fiscal years that end on the same day as the calendar year, most companies must report to the Securities and Exchange Commission by March 1st of the following year. This means there is a real push in each company to get the information out on time. Delays are symbolic of troubles. Top-notch companies always report on time.

Core Financial Statements

There are five core financial statements. These are common among all publicly traded entities. Each statement has a primary purpose and provides a lot of information. It is important for the reader to recognize that at this level of corporate sophistication, these statements are presented in a summary format. Additional details can be found in the auxiliary segments of the annual report. In addition, there are often supplemental financial statements breaking out a few of the more important financial components. The following subsections identify each report, its primary purpose, and provide an example. In addition, each subsection below will highlight one area every investor should look at first with each statement.

Balance Sheet

The balance sheet is a two-sided document. On one side (commonly presented as the upper half of the report) are assets. Assets are everything the company owns, from cash to legal rights. This ownership costs the company money, and the values presented reflect the ownership costs in dollars. Naturally, cash is self-explanatory. It costs a dollar to own a dollar.

The other side, typically the bottom half of the report, reflects the liquidation position if the company were to stop doing business at the moment the statement was dated. Most bottom halves of balance sheets reflect liabilities, outside creditors with superior rights to the assets, if the company were to cease operations. In addition, the bottom half states the equity position of the company; the estimated amount shareholders would receive if the company were to cease operations and liquidate.

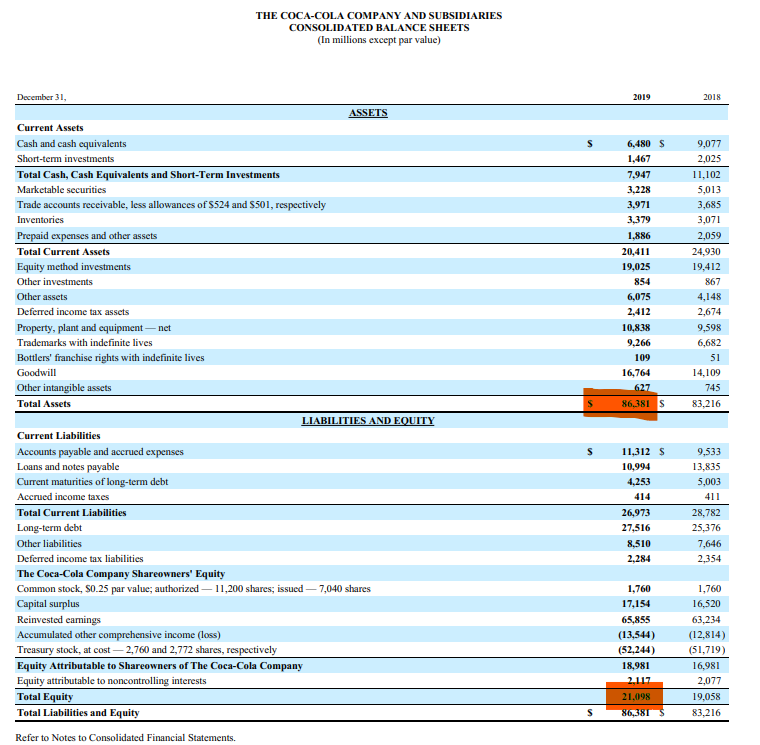

It is important to understand that the balance sheet’s primary purpose is to provide a statement of financial position at the end of the respective quarter or year. It is a lifetime to date report. As a company earns money, it accumulates these earnings in the ‘RETAINED EARNINGS’ account, which is a sub-account of equity. To illustrate, look at this simple balance sheet for Coca-Cola:

Notice two highlighted values. The first item is the total assets of Coca-Cola. They have $86 billion of assets. The second highlighted value reflects the estimated value all owners of the company, including shareholders, would receive if Coca-Cola were to cease operations and liquidate on that day.

Notice two highlighted values. The first item is the total assets of Coca-Cola. They have $86 billion of assets. The second highlighted value reflects the estimated value all owners of the company, including shareholders, would receive if Coca-Cola were to cease operations and liquidate on that day.

$21 billion of the $86 billion in assets is owned by these shareholders and non-controlling interests (explained in Phase Three of this program).

Take notice of the title and the date near the top. The values throughout reflect the lifetime cumulative balances in the respective accounts through the date of this report. Go down into the ‘The Coca-Cola Company Shareholders’ Equity’ section and find the line ‘Reinvested Earnings’. This dollar value reflects all earnings over the last 100 years (Coke went public back in 1919), less dividend payments made over the 100 years. It is the net amount the company retained for other purposes. You can see that the bulk of it is used to buy back stock (Treasury Stock) and cover other types of losses over the lifetime of Coca-Cola.

Basically, Coca-Cola returns its earnings to its shareholders by either paying dividends or buying back stock from shareholders. Remember, Coca-Cola is a DOW company and is considered one of the most successful companies in the world. Because it is a dividend-driven company, most buyers of Coca-Cola purchase the stock to hold it in a portfolio of dividend-based investments. Value investors only use dividend-driven companies as standards in their pools of investments. Now and then, the stock price may take a sudden deep price discount, and value investors will snatch up these types of companies, but this is unusual and unexpected.

For this lesson, the key is that whenever you look at a balance sheet, your very first step is to identify the ratio of equity to total assets. The higher the ratio, the more protected the shareholders are in their position in the company. In this case, the equity position is 24.4%. High-quality investments typically have more than a 20% equity-to-assets ratio. Here are just a few current equity-to-asset ratios for popular companies:

Disney – 41%

Apple – 20%

Microsoft – 39%

Bank of America – 11%

For the member, the key is that the higher the ratio, the more protected you are as an investor. Ideal positions are over 50%, but these types of investments are hard to find at good prices with publicly traded companies.

As for the balance sheet, it has two halves; the upper reflects assets, the lower a combination of liabilities and equity – amounts owed to third parties and the value for shareholders. Within the equity section sits a single account, which reflects the lifetime earnings to date, net of dividends paid, called retained earnings. Retained earnings are a function of net income.

Income Statement

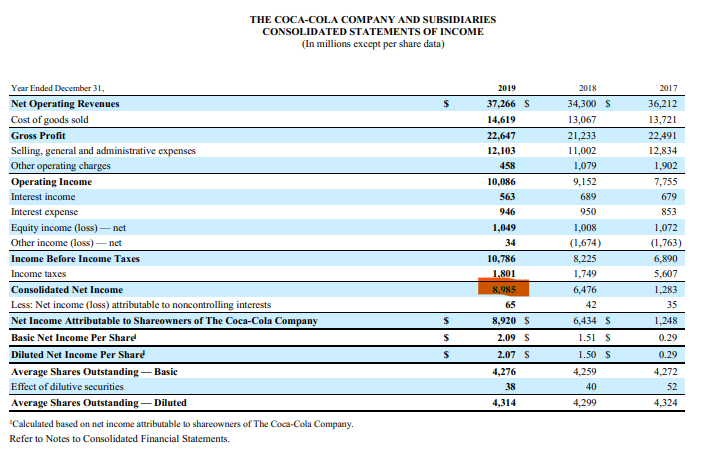

The income statement reflects amounts earned within a period. It is the most popular of all the financial statements. This doesn’t mean it is the most important; it is popular because this is where owners discover if the company is making money – ‘Profit’. Notice a key difference between a balance sheet and an income statement. The balance sheet reflects a lifetime to date status of the monies earned, a snapshot at a moment in time. The income statement is an incremental portion of the retained earnings. Go back to Coca-Cola’s balance sheet above. Lifetime earnings net of dividends paid out equal $66 billion. Look at Coke’s income statement for 2019:

In Lesson 8, five key financial points were identified, three of which are tied to this financial statement. The first identifies revenues. Notice the variances among the three years? Secondly, and reiterated several times in that lesson, is the importance of the gross profit margin. Look at Coke’s gross profit margin for 2019. It is an unheard-of 60% ($22.6 billion divided by $37.3 billion in sales). But it makes some sense; their products are not much more than water and syrup mixed, bottled, and distributed to consumers.

In Lesson 8, five key financial points were identified, three of which are tied to this financial statement. The first identifies revenues. Notice the variances among the three years? Secondly, and reiterated several times in that lesson, is the importance of the gross profit margin. Look at Coke’s gross profit margin for 2019. It is an unheard-of 60% ($22.6 billion divided by $37.3 billion in sales). But it makes some sense; their products are not much more than water and syrup mixed, bottled, and distributed to consumers.

The third important financial data point is, of course, the one that almost everyone likes to celebrate, and that’s net profit. It is highlighted in orange here. Coke earns $9 billion off of $37.3 billion in sales, net of all expenses, net of income taxes. This is an incredible 24% bottom-line net profit. This is one of the reasons why Coca-Cola’s stock price is so high in comparison to its book value. Every year, Coke does well. Look at 2018 and 2017. Immediately, several of you are saying to yourself, Well, 2017 isn’t that impressive. Look again. Look at how they paid almost three times their normal amount in income taxes. Why? Because Congress passed the Tax Cuts and Jobs Act of 2017, allowing major corporations like Coke to recapture historically deferred income and pay taxes now at a lower rate. Almost every major corporation took advantage of this reduced tax rate and paid taxes on deferred and overseas profits during 2017.

As a side note, look at the expense line called ‘Selling, general and administrative expenses’. This line reflects mostly the marketing campaigns that Coke utilizes to sell its products. When you see their commercial at halftime during the Super Bowl, that cost is included in that line right there.

Back to net income, the $9 billion in profit earned has dividends paid out to the shareholders. In 2019, Coca-Cola paid out $6.8 billion in dividends to shareholders. This means the difference, $2.1 billion, is accumulated in the ‘Reinvested earnings’ account on the balance sheet. Thus, of the $66 billion of reinvested earnings, $2.1 billion of that is from 2019’s profits.

There are two important lessons here with income statements. First, it identifies the net profit of the company during a short period in the life of the company. The periods are either during a quarter of a year or for the entire year. Secondly, the income statement customarily puts forth three of the five critical financial data points explained in Lesson 8. It just so happens that Coke also reports the fourth important data point of earnings per share in its income statement. Thus, during 2019, Coca-Cola reported that the company earned $2.09 per share. There are 4.3 billion shares in the market.

To have a more detailed understanding of how the earnings were allocated, a third financial statement is prepared – Statement of Retained Earnings.

Retained Earnings

Retained earnings are a corporation’s financial statement term reflecting the net balance of all earnings during the corporation’s life. It reflects the net amount after paying out dividends and other preferred positions in the equity section of the balance sheet. The equity section of a balance sheet is divided into three major groups. The first group is preferred positions of ownership, often referred to as ‘Preferred Stock’. These are owners with a superior position for earnings, but they gave up the right to vote for control purposes to gain this preferred position in receiving earnings. The second group is the actual shareholders, the owners who have the right to earnings and have the right to vote their shares when appointing board members. The third group is called ‘Minority Interests’. These are often small positions held in subsidiary corporations. In most cases, they are individuals or a management team that is a part of a joint venture or some partnership with the subsidiary company. These minority interests only have the right to vote on their position with the subsidiary company. The mother corporation owns the majority stock position of the subsidiary and, in general, controls the subsidiary. However, these lesser shareholders still have a right to their share of their company’s respective earnings, which is included in the overall corporation’s ‘Comprehensive Income’.

This exists with Coca-Cola. Coca-Cola has multiple subsidiaries in many different countries throughout the world. In the U.S., Coke has partnerships with many distributors and packaging companies (the actual bottlers of the product). In addition, Coke has purchased multiple brands of products. For example, they own Minute Maid, and this company has its distribution deals, plants, and rights to transport the product. Thus, when you look at Coke’s income statement, remember that comprehensive income includes all these other subsidiary companies.

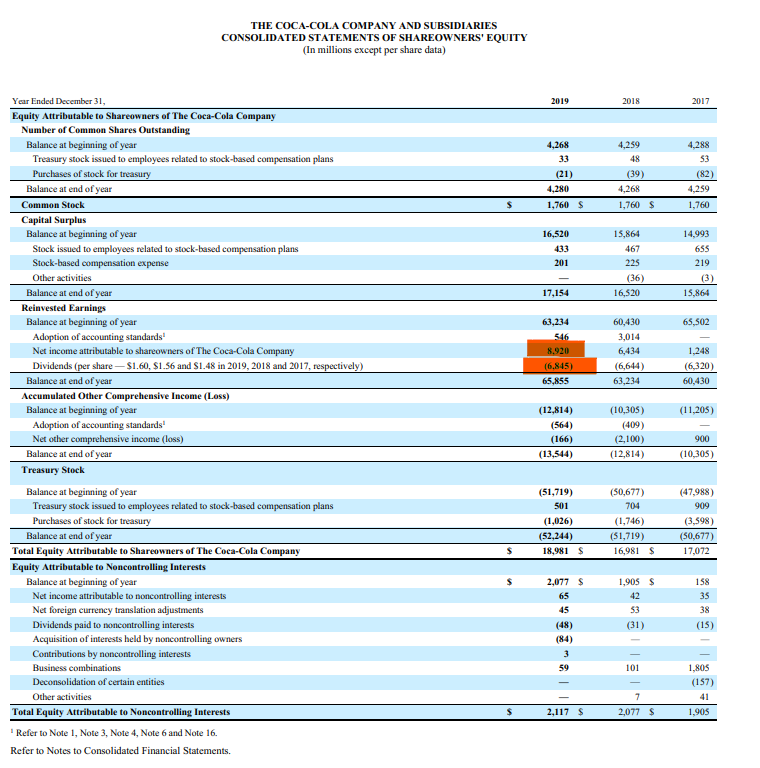

To ensure that readers of financial statements are not misled about the net profit, a statement is issued explaining how this net profit is allocated to the respective ownership groups in the organization. Here is Coca-Cola’s retained earnings statement, which they call the Consolidated Statement of Shareholders’ Equity. They are effectively explaining the equity section of the balance sheet in more detail.

Look at how this breaks out. The report is divided into two sections reflecting two groups of ownership. Coke does not have a set of ‘Preferred Shareholders’ and, as such, only has two groups. The first section is for the primary owners, the shareholders.

Look at how this breaks out. The report is divided into two sections reflecting two groups of ownership. Coke does not have a set of ‘Preferred Shareholders’ and, as such, only has two groups. The first section is for the primary owners, the shareholders.

Look at the title of this section – Equity Attributable to Shareholders of The Coca-Cola Company. It starts by identifying the number of common stock shares. Recall from various business lessons in your life that common stock has three traditional values comprising its total value. First is the legal value for a corporate organization, which is simply called common stock. Next are the original amounts paid to the company more than par value (the legal value), and Coke calls this ‘Capital Surplus’. Now, for the third financial value of the stock, the lifetime earnings value. Here, the company starts out with a beginning balance of $63 billion and has to adjust this value due to some accounting changes – legal requirements. Thus, they add half a billion dollars to the total. Then comes the net profit from the income statement. From this net profit is deducted by the dividends paid during the year. Remember, on the income statement, Coke earned $2.09 per share. Look at the per-share dividend payments for 2019. Coke paid out $1.60 of the $2.09 earned per share. Coke is one of the more dividend-friendly stocks in the market because they do pays out more than 70% of its net profits year after year. Most companies do not pay out more than 50% of their net profits.

The two highlighted values reflect the discussion points from the income statement section above. Net profits and the amounts paid out in dividends contributed $2.1 billion towards the cumulative lifetime to date balance of reinvested earnings of $66 billion.

The report continues by breaking out comprehensive income issues, treasury stock values, and finally, the total amount attributable to the shareholders of Coke. These are the owners who have the right to vote their stock for management purposes.

The second section is the dollar values associated with minority interests. Take note that although their position is only $2 billion of the combined $21 billion of equity (review the balance sheet above), it is significant enough that it must be reported separately with this financial report so that voting owners (traditional shareholders) can determine the proper allocation of the entire equity of the company.

In Phase Two of this program, this particular report is explained in more detail, and several illustrations demonstrate how to interpret the information as it relates to value investments. For this lesson, it is introduced to the idea that the most important data point is cumulative lifetime earnings and how the current period of activity contributes to this lifetime value. This also makes the connection between the income statement and the balance sheet.

These first three statements tie together how the company performed and where it stands financially. But another report is required to explain how the cash position of the company changed during the year. Look again at the retained earnings above. The net increase of $2.1 billion is impressive. Novice business investors would jump to the conclusion that the difference must be in the form of additional cash in the bank account. This is not the case. Investors want to know how this $2.1 billion was used; if not all of it ended up in the bank account. The cash flows statement explains how this difference is used.

Cash Flows Statement

This one particular financial statement is more misunderstood than any other report. For those not trained, it can be very confusing. This lesson introduces this particular statement and how to properly interpret the information from an overall viewpoint. But before it is introduced, let’s first recap Coca-Cola’s financial information as presented thus far in this lesson.

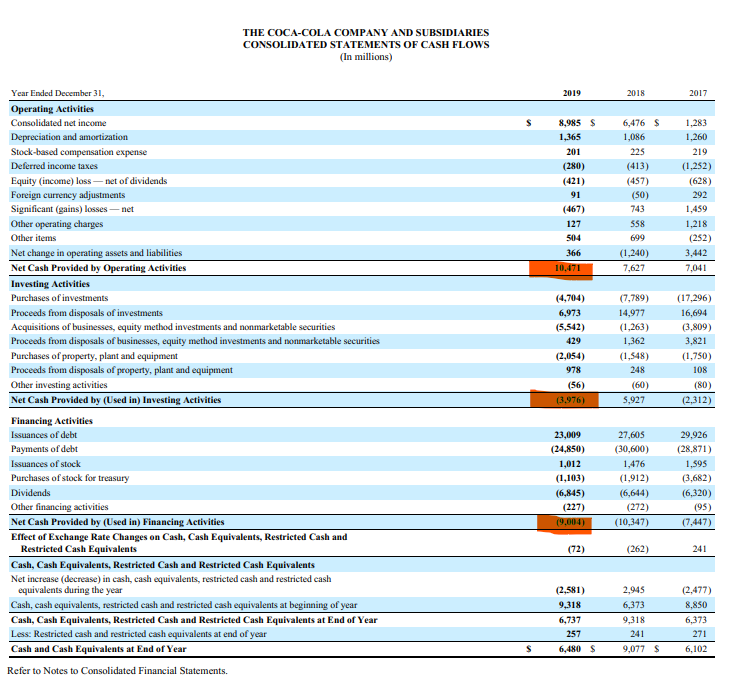

From above, Coke generated a profit of $8.9 billion. With these earnings, it has certain obligations. First, Coke must pay any legal obligations, such as debt instruments, including principal on debt, no differently than a small business must make its monthly payments for its mortgage or transportation notes. Every note payment has two components: interest and principal. Interest is a deduction on the income statement. Principal payments merely reduce the obligation on the balance sheet. Go to the balance sheet under the liabilities section and notice that Coke has long-term debt of $27.5 billion. During 2020, a small percentage of this $27.5 billion is due back to the lender in the form of principal, along with the interest payable.

Secondly, Coke wants to pay its shareholders their risk reward. As illustrated above with the consolidated equity statement, Coke paid $6.8 billion in dividends.

A third use of these proceeds is to expand the company. Just like any other well-run organization, Coke does not want to lose its position with non-alcoholic beverages worldwide. Therefore, it needs some capital to reinvest in potential new products or expand operations in other countries, and so forth. This is commonly referred to as investing to not only maintain a company’s economic position, but to expand it as well.

Finally, profits are used to reduce other debts, such as current liabilities, or even buy back some of the common stock to buttress the market value of existing stock.

Whatever the difference is, the effect is on the cash account. Realize, it is possible to spend more than one earns in a given period, and this reduces the cash in the bank.

Now, let’s look at what happened with Coca-Cola in 2019.

Every cash flow statement has four distinct sections.

Every cash flow statement has four distinct sections.

The first section is located at the bottom of the report; the author has no idea why the accounting profession advocates placing the first section at the bottom.

Anyway, it basically reflects the change in the overall cash position of the company during the fiscal period of the report. In this case, Coca-Cola started the year with $9.3 billion in its bank accounts. It ends the year with $6.7 billion in its bank accounts; thus, it spent $2.6 billion of its cash plus the net profit it earned (almost $9 billion).

Where did all this money go?

It gets worse. Go to the very upper section entitled ‘Operating Activities’. Notice that the very first line reflects the net income of the company. This is always the starting point for every cash flow statement.

For those of you not aware, the net profit includes accrual adjustments, which are often non-cash in nature. For example, the largest adjustment is always depreciation. Coca-Cola takes a depreciation/amortization expense in 2019 equal to $1.4 billion. There are some other lesser value adjustments listed there, but for most companies, the biggest non-cash adjustment is depreciation. Depreciation was deducted in the income statement; therefore, for cash purposes, it is added back.

The net effect is that the cash income produced from regular operations equals $10.5 billion.

Thus, what this means is that the company spent this $10.5 billion along with an additional $2.6 billion of cash from its bank accounts; therefore, in the aggregate, it spent $13.1 billion during 2019. How on earth can a company spend $13.1 billion? Let’s find out.

From above, it is stated that the first requirement of a company is to pay its legal obligations, i.e., its long-term debt principal as agreed in the various loan documents. This is reported in the third section of the report called ‘Financing Activities’. The very first line states ‘Issuances of debt’; these are the amounts borrowed. Notice it is a positive number, which means cash came into the company. The second line is the one we are looking for. Payment of debt was $24.9 billion. This means Coke paid out $1.9 billion more than it borrowed from creditors.

Go down a little further, do you see the big payment for dividends? It matches the amount as reported in the consolidated equity report. In effect, Coca-Cola pays down its debt $1.9 billion and pays out to owners another $6.8 billion. Altogether with the other minor amounts, Coca-Cola paid $9 billion to address financing issues. There is one other minor adjustment, which reflects $72 million for the effect related to currency rate changes. Notice this is a negative value. This leaves $4.0 billion for the third purpose of earnings: expanding the scope of operations to maintain economic or improve the company’s overall economic position.

In accounting, we call this ‘Investing Activities’. This is the second section of the report. It identifies where Coca-Cola spent some of its money to expand its economic position. The main line item is acquisitions of businesses for $5.5 billion. This is Coke going out and buying up distributors and purchasing certain rights for certain products. In 2019, Coca-Cola paid $4.9 billion for a company called Costa. Costa is a coffee company with retail outlets in 30 different countries. Coca-Cola decided to expand into the hot beverage side of the non-alcoholic beverage business. This makes sense; it wants to compete with Starbucks and the other big coffee retail operations. This is the reason Coke spent some of its cash. Altogether, Coke spent $4 billion on investing, including $4.9 billion for Costa and another $2.1 billion for production facilities. It cashed out some of its existing investments to assist with the purchase of these new assets.

To help you comprehend this a little more, go back up to the balance sheet. Look at how Goodwill increased from $14.1 billion to $16.8 billion in one year. This goodwill increase is a reflection of the amounts paid over book value for Costa.

Now let’s put this altogether in a little summary report:

*All values are in Billions of Dollars

Net Profit $8.9

Non-Cash Adjustments from Operations Section 1.6

Cash Position Increase Due to Operations $10.5 (ties to Operational Cash Flow)

Cash to Expand The Company’s Economic Clout (4.0) (ties to Investing Cash Flow)

Cash Used to Pay Down Liabilities (2.1)

Dividends Paid (6.9)

Change in Overall Cash Position ($2.5)

Currency Exchange Adjustments (.1)

Overall Cash Position Decrease ($2.6)

Again, the top three driving forces of money being spent are 1) dividends paid, 2) the purchase of Costa, and 3) paying down debt.

One last note, remember from Lesson 8 that there are five key financial data points. The last of the five addresses cash from operations earned per share. This is simply:

Operational Cash Flow = $10.471 Billion = $2.45 per share

Number of Shares Outstanding : 4.28 Billion Shares

As stated in Lesson 8, cash earnings from operations per share should always exceed net earnings per share. From above, net earnings per share were $2.09. Thus, Coca-Cola does indeed generate more cash per share than it earns, and this is tied to the additional non-cash depreciation deduction getting added back to net profit.

During Phase Two of this program, the value investor member is provided multiple lessons on how to read the cash flows statement more comprehensively and tie the information to the balance sheet. In addition, in Phase Three of this program, the value investor is trained on cash flow statements for the respective pools of investments. Remember, each industry is different. Some industries keep their cash flow statements simpler than Coke’s; others can be quite convoluted, and it takes some additional understanding to interpret this information.

But most importantly, the changes that do occur with the four above statements are explained in detail in the report of financial statements called ‘Notes’.

Notes

The devil is in the details. The notes to financial statements offer deep insight into the respective reports and certain key information. Typically, larger corporations often have more than 50 pages of notes and key supplemental schedules. With Coca-Cola’s annual report as delivered to the SEC, there are 23 notes covering 65 pages.

Most of the notes cover standard required pieces of information, such as:

A) A summary of significant accounting policies is presented. This is especially important with really large conglomerates like Coca-Cola. The accounting function has a bearing on how financial information is presented, and any changes can influence how an investor values the organization.

B) How long-term debt is allocated and accounted for over time, including any pertinent parts of the respective bonds & notes.

C) Several notes address the company’s pension plan. Often, pensions are a source of hidden liabilities, as accounting for them is constantly changing in order to better identify these hidden liabilities.

D) Foreign investment is covered, which helps to identify risks for value investors. A good example is an investment with China; given the contentious diplomatic relationship between the two economic powerhouses in the world, it is critical to limit exposure to China.

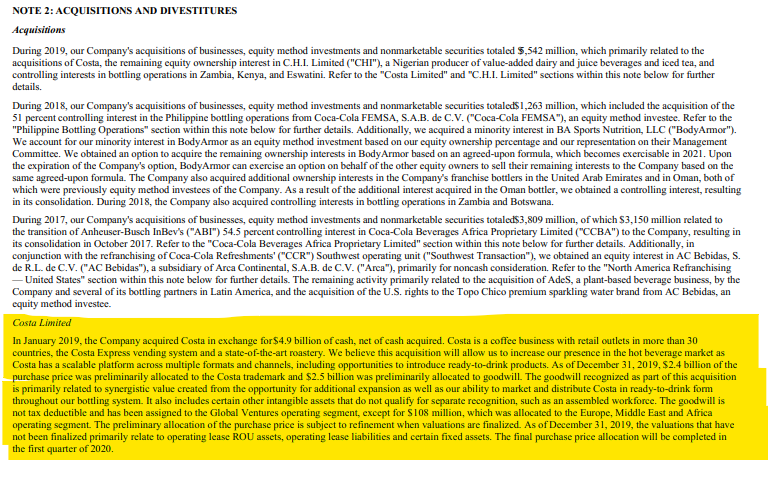

Notes are pretty easy to read and understand. They clarify the financial information reported. Here is just one page of the four pages dealing with Note 2: Acquisitions. The area highlighted in yellow is about Costa.

If you read it carefully, it provides two interesting tidbits of financial information. The first is on line 4 about midway. It says that $2.5 billion of the $4.9 billion was allocated to goodwill. Remember, up in the balance sheet, goodwill’s balance at the end of 2018 was $14.1 billion, and at the end of 2019, it increased to $16.8 billion. This $2.7 billion increase is mostly attributable to the purchase of Costa.

Just before that part, it says that $2.4 billion of the $4.9 billion is allocated to trademarks. Just as with goodwill, the balance sheet states that the trademark balance on 12/31/18 equaled $6.7 billion, and on 12/31/19, it increased to $9.3 billion. This change is $2.6 billion, driven by the $2.4 billion allocated to Costa.

If you were an investor with a hold position on this particular stock, e.g., you purchased it at a good price and are strictly interested in the high dividend payout, the acquisition of a United Kingdom company in the hot beverage industry would be something you would want more information about. How is Coca-Cola going to develop this, especially in the United States? What are the forecasted earnings and sales?

As a value investor, your concern may be more in line with risk exposure. Could this investment cause a sudden market price dip in the stock price?

Notes add a lot of value with interpreting the respective lines of information on the first four reports. Furthermore, notes fill in the blanks for certain parts of each report. If a note is written for a particular item, it is identified with a numerical code on the respective report, and that code ties to the particular note in the Notes section of the annual report.

Altogether, Coca-Cola’s annual report to the SEC is 214 pages long. It is filled with supplementary schedules, comments from the management team, write-ups about the respective operations, and how the company makes its money. With value investors, this information is read once a year when the new report comes out, just to ensure that the company didn’t make significant changes that would impact the buy/sell decision model developed for that respective company.

Coca-Cola is not currently an investment potential in any of the Investment Fund’s pools. There is no non-alcoholic beverage pool of companies. For those of you just learning about value investing, value investors use pools of similar companies in a single industry. Value investors may have upwards of five pools with about 30 to 40 different potential stock investments.

Join the Value Investment Club This site's Value Investment Club (Membership Required) utilizes a Value Investment Fund model with an annualized 23.3% return over a SIX and THREE QUARTER-YEAR history. It has grown from a starting basis of $100,000 and is now $411,989 before taxes of $91,166. This is a 19% annualized return after taxes. Membership provides instantaneous access to time-sensitive information. Membership provides: Value investing, in its simplest terms, means buying securities at a low price and selling them at a higher market value. Value investing is defined as a systematic process of purchasing high-quality stocks at an undervalued market price, quantified by intrinsic value and justified through financial analysis, then selling the stock promptly upon market price recovery. Membership gives the reader full access to all information on this website. Act on Knowledge.

Pertinent Bits of Information – What Value Investors Want to Know

Other than the five important financial data points, what else would a value investor want to know, and how is it found in the annual report?

The key is the respective industry in which the company belongs. Each industry is different. Always think holistically first. What exactly does this industry do to make money?

For example, one of the pools the Value Investment Fund currently uses is the banking industry. Banks want a volume of customers to deposit money into their bank, and in turn, the bank lends this money out to third parties. The bank earns interest and pays out a little bit of interest for the use of that money. They also borrow money from other parties to lend out. A common fear among banks is that when they lend money out, the borrower will be unable to pay it back. Thus, how much is set aside to cover potential loan losses? Another important piece of information would be the spread differential between interest receipts and interest paid to deposit accounts at the bank. This spread is the net money earned to cover all the expenses of the organization. Are there other sources of earnings? Where does this come from?

The annual financial reports of banks clarify this and answer these pertinent questions. Again, each industry is different, and therefore, what is important to understand changes with each industry. Thus, there is no universal question that will encompass all industries. Value investors acknowledge this when they create their pools of potential investments. They create a key set of questions to ask that pertain to all potential investments in that pool. The answers are compared, and it becomes easy to recognize the better operations in that pool. It is these companies that value investors desire and often slightly modify the buy/sell model in order to take advantage of that company’s better overall financial status and risk position.

This entire concept is covered in more detail in Phase Two of the program and already exists for the current three pools of investments advocated by the Value Investment Fund. In order to access any information related to the three existing pools, the reader must be a member of the club. Act On Knowledge.