Value or Growth Investing

Which is the Superior Investment Strategy?

“An investment in knowledge pays the best interest.” – Benjamin Franklin

There are about a dozen popular investment strategies. Two of them stand out in the crowd as the best due to similar standards of research required; they are value and growth investing. From these two top-tier investment methods, which investment strategy is superior, value or growth investing?

Many who are unfamiliar with investing consider value and growth investing as synonymous. The truth is, both are starkly different. First, both have completely different approaches towards risk. Secondly, one places greater emphasis on holding the investment for extended periods of time. A third difference relates to the reliability of the supporting information when researching the potential investments. Finally, one of the methods has a superior dividend payout ratio over the other.

This article will delve into these four distinct differences and how they play into results. When done, the reader should be able to quantify the value each provides, depending on the mindset of the investor. Before getting into the four core differences, readers should understand the emphasis each form of investing has to discriminate between the four core differences.

Value or Growth Investing

Different Concepts of Investment Strategy

Investment strategies have different concepts that accrue wealth. Many strategies place some level of reliance on speculation. These strategies never use the term speculation, as those who advocate the strategy firmly believe there is a learned basis to justify the respective strategy. A perfect example is ‘Day Trading’. Day traders are passionate that patterns exist. Any well learned business major knows that patterns in business and economics can’t possibly exist within 24 hours.

To reduce the level of speculation involved, two of them require extensive research before the commitment of a capital investment. Both value and growth investing require a deep understanding of financial, economic, and performance standards prior to making an investment decision. No other investment strategy is founded in research to the extent these two methods implore upon those who exercise these methods. So if both require extensive research, how could they have a different mindset about investing?

If the reader were to look at the financial results of both methods over the last century, one would discover a similar strong pattern of good returns and, in many cases, exceptional returns. These two methods outperform all others by dramatic outcomes. Again, this is directly due to the emphasis placed on research and conducting financial analysis when making investment decisions. Although both rely on extensive research, there is an undeniable difference that exists between value and growth investing.

Growth investing is grounded in finding young emerging companies that have immeasurable opportunities to grow. Imagine if someone came to you in the late 80s and said to you that you should buy Microsoft Inc. Knowing what you know today, you would have sold everything you own to get in on the ground floor. There are 10’s of examples of exceptional outcomes with many companies over the last 40 years. Granted, many of them are in the technology sector of our economy, but the truth is this: these companies demonstrated unheard of growth over the last 40 years.

This concept still exists today. What if you could invest in the next Microsoft or Facebook? To do this, one would have to conduct extensive research and analyze the company’s performance to date to determine if growth will far outpace the economy in not only the near future, but for a long foreseeable duration. An investment today will reap outstanding rewards many years from now.

Value investing’s concept is distinctly different. Just like growth investing, value investors place a tremendous amount of emphasis on research, too. But this is where the two investment strategies separate. Value investors utilize systematic buying and selling of certain companies. Value investors simply buy high-quality quality well-run companies when the securities’ price drops well below intrinsic value and then simply wait for the market price to recover to reasonable, acceptable prices and then sell the security. Value investors make their money on the delta and, in the interim, receive dividends. There is no allegiance to some economic driver to improve the market price of the respective stock. The simple truth is this: the respective investment is a highly stable, well-run operation, and there is very little to no chance the consumer or customer’s buying habits are going to change and therefore impact the core underlying value of the company. Value investors key in on the company, not the potential market for increased share or market growth.

Value investors stick to a very simple mantra of buy low and sell high, in good quality companies. Growth investors buy new companies that they firmly believe have a tremendous amount of potential for an extended period of time (years) in a growing industry, and in turn, the company’s securities will follow this growth rate.

Notice right away the distinct differences. Value investors have no interest in a long-term investment with any company; growth investors invest and hold for years. In addition, value investors place a lot of emphasis on highly stable, well-run operations; growth investors invest in young companies and many cases, new products. The result is still the same desire, to get a good return on one’s investment on an annual basis.

With this difference in how to get a good return on one’s investment, the reader must now look at the four core principles that separate the two mindsets of investing.

Value or Growth Investing

A Different Approach Towards Risk

In business, risk is defined as exposure to financial loss and, in rare cases, financial ruin. Value and growth investing both have similar and different beliefs related to risk. First off, both dramatically reduce risk by researching and selecting ‘QUALIFIED’ opportunities for investment. But this is where they diverge. Even with good research of not only the company for investment, the respective economic industry, and the products involved, once a growth investor decides the particular company is worthwhile, the investment is made, no matter what the market price is for that particular security. There’s no waiting around for the price to drop or change in any way. They key in on the premise that future growth is so dramatic, any change in the near term, whether up or down, is immaterial to the long-term return on the investment. Thus, growth investors accept short-term risk that the respective security could drop dramatically (> 5%) in price.

Value investors take a whole different approach towards risk. Eliminating risk is their number one priority. The emphasis on risk reduction is so ingrained in the mindset of value investors, it is done through a three-step security selection process.

- Risk is dramatically curtailed by only selecting from among the top 2,000 companies in the world. This particular website’s Value Investment Fund only selects from the top 2,000 companies in the United States. Why the top 2,000? The answer is simple: the top 2,000 are there at this tier because they are highly stable, well-run operations. They rarely lose money and have outstanding upper and mid-management personnel and systems. They hire the elite out of the top schools; they have extensive training and require their managers to gain experience before allowing them to make decisions. These companies exercise superior policies related to all facets of operations. The chance the company will experience setbacks of any kind is pretty much eliminated.

- Risk is further minimized by only investing in companies that are demonstrating continuous growth. Any top 2,000 companies that have experienced setbacks during the last three years are eliminated from the opportunity pools. In addition, value investors group similar companies into pools. These pools of certain industries allow the value investor to gain a better understanding of what works and what doesn’t work among the members of a particular pool. In effect, there is a standard bearer within each pool that demonstrates superior performance. All other members are gauged and graded against this superior operation. As an example, with this site’s Fast-Food Restaurants Pool, McDonald’s is the standard setter. All other potential investments in that pool are gauged against McDonald’s.

- Once research is completed, a potential investment’s intrinsic value is calculated. Intrinsic value is the core, universally agreed-upon value per equity position. Intrinsic value sets the baseline of financial worth for the respective member within a pool. With a baseline of worth established, a value investor adds a margin of safety by setting the buy price lower than intrinsic value, in almost every case at least 5%; in some cases, the buy price is more than 20% lower than intrinsic value. This added margin of safety eliminates risk. Yes, the value investor understands that they could purchase a position in a company at a very good price, and yet, the market price could continue to fall for that security. Research assures that this dip in price is unsustainable and in a very short period of time will return to the buy price and most likely improve to intrinsic value. This practice of including a margin of safety practically eliminates business risk.

Take note of the two different approaches towards risk management. Growth investors understand and ACCEPT the risk associated with immature operations’ policies and an inexperienced management team. Value investing has ZERO tolerance for risk. Yes, odds are that other companies in this same business sector/industry will also have inexperienced management teams simply due to the relative newness of the industry or products produced. Growth investors accept this risk as a function of practice and include this in their expected return on investment.

Furthermore, the historical financial performance of growth companies has much shorter look-backs with time, and they rarely have extended windows to demonstrate financial success. These companies are in the penny stock and small-cap tiers of market capitalization. Growth investors key in on the fact that there is unlimited growth for these companies for an extended period of time and that this growth, although it comes with greater operational costs, will easily cover the costs of transitioning towards a well-run operation.

Finally, for growth investors, the current market price is irrelevant. The fact is this: this particular company has been identified as a pure opportunity for shareholders. The overwhelming strong growth over the next few years will outpace any short-term setbacks with market prices for the security. In effect, the current market price is irrelevant.

Value or Growth Investing

A Different Mindset Related to Holding the Investment

By now, the reader should be able to deduce the difference between the two investment strategies related to buying and holding the investment. Growth investors hold the investment for extended periods. With many buys, holding periods are expected to last at least seven years, in rare cases, more than 10 years. The universal thinking, though, is at least two years, and the most common holding period is more than three years, with a medium of at least five years.

Value investors are interested in the shortest holding period possible. Ideally, one day is desired. Who wouldn’t want to buy a stock low, and the next day the stock soars to its market price? Since this is unrealistic, what is the mindset of value investors?

Value investors seek out good buys whereby the market price will quickly recover to prior market highs for that company. In general, value investors seek out investments with recovery periods of less than six months and are willing to wait up to two years for the market price to recover to a reasonable and desirable sale price, which then ensures a good return on one’s investment. This site’s Value Investment Fund has only had one particular set of buys that have taken more than one year to recover to the predetermined market price. For those of you new to investing, the longer the holding period, the more likely the annualized return on one’s investment decreases. The return on investment formula is a function of time and change in price; the longer the period to recover, the lower the overall return.

Growth investors think differently; they know it will take time for the company to achieve its goals and, in turn, acquire improved results with the market price for the respective securities. The market has demonstrated time after time that those companies with viable long-term growth get remarkable market price increases for their securities. In effect, the market is driving the price high today for future potential. This is a big driving force as to why growth investors want to get in on the ground floor of this high-rise potential. Often, the market price increases such that there are unheard of price-to-earnings ratios for the particular stock. A good example is Chipotle Mexican Grill Inc. After it went public 20 years ago, the market price peaked in the summer of 2021 at 190 times earnings. This is what growth investors dream of for their investment.

In summary, growth investors hold their investments for at least two years and, on average, more than five years. Value investors have a much shorter window related to the hold period. The common maximum holding period for value investors is two years. On average, most investments have a full cycle of buy and sell in less than one year.

Value or Growth Investing

Depth of Information

Coca-Cola has been around for over 100 years; since 1919, it’s been traded in the market. During those last 102 years, it has never lost money. That is why today, it is a Dow-rated company. Similar to Coke are the other 29 DOW companies. All of them have extensive histories of financial reports, annual reports, and supplemental information for investors. This extends to the other top 2,000 companies in the United States. Only a few dozen have a limited history of activity to augment the information available. Thus, value investors have a distinct advantage over growth investors. Value investors have a wealth of data to analyze and support their decision models. Growth investors don’t have this depth of information.

Growth investors must resort to other sources of information to form a decision matrix for their investments. They have to rely on industry information or recent articles written by credentialed individuals to have valid information from which to form an opinion. Notice the similarities and distinct differences between the two investment approaches. Both require extensive research; however, value investors can get their information straight from the company they are investigating. Whereas, growth investors must resort to other sources in order to augment information provided by the potential investment. Growth investors must do a lot more legwork in order to gain the level of confidence necessary to make the investment.

Value or Growth Investing

Money in the Bank, Dividends

Very few of the top 2,000 companies avoid paying dividends. Many of the top companies have strong payout ratios against their earnings. Coke is an example of a company that pays out more than 80% of its earnings as dividends. Whereas, Chipotle Mexican Grill Inc. (a perfect model of growth investment strategy) has yet to pay a single penny in dividends. In general, most of the top 2,000 companies pay out more than 25% of their earnings as dividends. This dividend payout improves the return on investment for value investors. Since value investors minimize risk by buying at extremely low market prices, the dividend yield improves dramatically. For example, McDonald’s current market price (late March 2022) is around $250 per share. Its annual dividend is just over $5.50 per share. Thus, its current yield is approximately 2.2%. The current intrinsic value for McDonald’s is less than $185 per share, and the buy point is currently set at $162 per share. At $162 per share, the dividend yield improves to 3.4%. This is an excellent yield for a stock. An acceptable yield is 2.8% to 3.1%. Thus, prices in the $177 to $196 range are considered acceptable, but not exceptional.

With most value investment-based transactions, dividend yields exceed 2.5% per share. This is highly desirable. Thus, while holding the stock, the value investor earns outstanding yields via dividends. It is like icing on the cake for one’s investment.

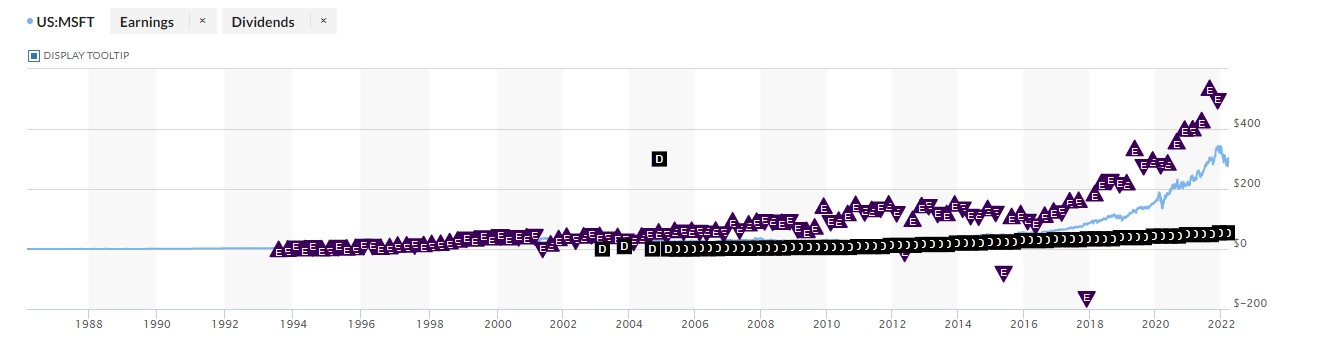

Growth investors don’t get this advantage. There are hardly any, if any, growth-based companies that pay a dividend. Earnings are strictly retained to fund the growth of the company. Look at Microsoft’s early years of earnings compared to dividends:

It took 18 years of retaining earnings before the company paid its first dividend. It took almost another four years before it paid dividends regularly. Growth investors must endure this ‘no dividends’ form of financial performance related to their investment. However, it is often rewarded with an increased market price per share.

Both methods acquire real wealth from the price change in the market for the respective security. For value investors, dividends are just an additional boost to their share price change.

Summary – Value or Growth Investing: Which is the Superior Strategy?

Without a doubt, these two investment strategies outperform all other investment methods. The primary reason for their superior performance, both require extensive research and construction of well-grounded decision matrices. They are simply the two best methods to earn a return on one’s investment.

However, with value or growth investing, both have distinct differences related to how risk is managed. Value investing minimizes risk by only investing in top-performing companies with long, stable histories of financial results. In addition, risk is reduced by comparing the potential investment against standard bearers within that industry. Finally, buy points are set with a good margin of safety below intrinsic value. Growth-based decisions ignore this risk aspect because they rely on the consumers’ purchasing habits and that this particular product/service line will continue to expand, thus providing the opportunities to invest in companies that are going to take advantage of these broadening markets.

In addition to the difference tied to risk, both have different holding periods for their investments. Value investors rarely hold an investment longer than one year, while growth investors average more than five years holding the security prior to selling it to make their money.

A third difference exists in the depth of information about the company. Value investors only invest in companies that have been around for more than 20 years. Growth investors are taking advantage of limited information and using alternative sources to form a basis to make a buy decision for a company.

Finally, the particular companies for the investment have different approaches to utilizing earnings. Valve investors are buying companies that reward shareholders by paying dividends regularly. Growth operations need these earnings to continue funding expansion. Growth investors rarely receive dividends from their investments.

Given these differences, the question remains, which is the superior strategy, value or growth investing?

While reading this article, the reader should have taken notice of something intriguing. Early on, it was noted how research reduced risk dramatically for both methods. Other methods have differing levels of research but rely on some degree of speculation when making their buy/sell models. The less research involved, the greater the reliance on speculation to earn a good return on the investment. Both value and growth investing reduce speculation dramatically by taking investing to another tier of performance. Both value and growth investing have proven histories of outstanding returns. Some growth-based indices have demonstrated returns over 18% annually for extended periods of time, more than 15 years. Those that are well managed and have deep research into the potential investments have averaged more than 18% on average per year for more than 20 years in a row.

Whereas value investing has had similar returns over a much longer time frame. Some years, value investing beats growth investing by significant margins. Other years, it’s the other way around. So again, which one is superior?

Go back to the concept of speculation. Value investing tries to eliminate speculation as much as possible. Speculation is the dagger of any investment fund. With growth investing, there still exists some speculation. Growth investors take additional risk by believing the particular industry or product/service will continue to grow faster than the overall market as a whole. In addition, there is an increased risk of holding the investment for a longer period of time. It is quite possible that the consumer will suddenly discover fault with the product, or it will fall out of favor with the public. A good example was ‘MySpace’, the precursor to Facebook. Furthermore, reliance on alternative sources of information adds to speculation. Finally, in business, particularly investing, payment of dividends is a company’s way of saying ‘We made it’. Dividends demonstrate solid operations and performance, both with product and financial results.

The speculation aspect of the difference between the two methods gives a slight advantage to growth investing over value investing, tied to the old risk/reward aspect of investing. Although the lifetime concept of growth investing is still young at just over 50 years, the remarkable average returns are undeniable. Value investing has a longer history and, with this, reliable consistency. And if you think about it for a moment, it makes sense. There is a greater risk with growth investing than with value investing, due to the marginal aspect of speculation; thus, the financial return is also going to be greater. But again, the only reason growth investing is successful is due to research into the particular industry.

However, value investing is substantially lower in risk and almost gets comparable returns to growth investing. This is important; growth investors must do extensive work in order to make good decisions. Value investors build an initial model and simply update the model annually. With value investing, there is less work, less risk, and just slightly less return on one’s investment in comparison to growth investing. This is what smart investors seek. It isn’t always about a great return; it’s about a GOOD return with as little risk as possible.

Think of the hierarchy of risk/reward related to investing. Without a doubt, both methods stand out over all other methods of investing. Growth investing has demonstrated a great return on investment, but this includes a significant increase in risk of loss. Value investing has demonstrated good returns year in and year out without much risk involved.

Which one is superior? It just depends on your risk acceptance level. Smart investors always want to reduce or eliminate risk as much as possible. This is why government bonds are the number one preferred investment in the market; government bonds have no risk. If one can get really good returns without risk, then there is no doubt, this is the preferred form of investing.

Value investing is the superior investment strategy. Act on Knowledge.